What are the implications of Facebook Pay?

Facebook finally unveiled its plans for an integrated payment solution similar to Snapcash by Snapchat, WeChats integrated payment solution and Kakao Pay from Daum Kakao. The rumors of Facebook entering the payment space has been going on for a while, ever since Facebook obtained money transfer licenses almost a year ago. The hiring of former Paypal president David Marcus as head of Facebook Messenger. Lastly, TechCrunch published hacked screenshots of Facebook Pay october last year. This should by other words not have come as a surprise for anyone. But will this be another Slingshot-moment (anyone else remember this?) where Facebook are accused of copying Snapchat? Here is my opinion on why Facebook has a unique position when it comes to P2P-payments.

P2P-payments rely on trust. Users have already entrusted facebook with almost every detail of their social circles and interests. Most Facebook users use their real name as an identifier which adds another layer of trust.

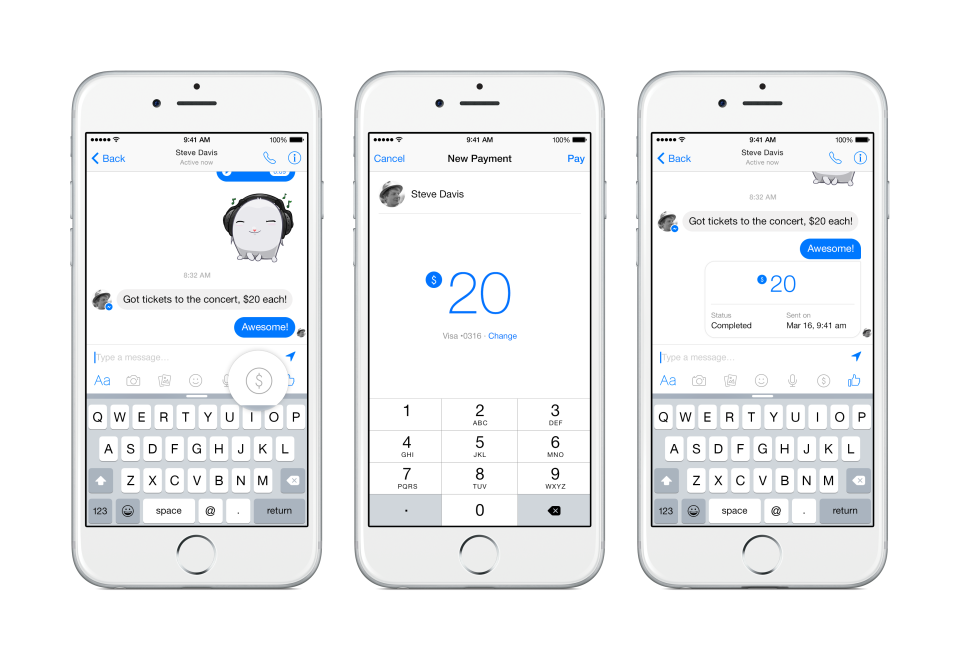

It is convenient. Bank accounts and credit card numbers are made for ledgers and core banking solutions, not people. Facebook connects P2P-payments to a relevant context, which is often a conversation. According to Facebook, conversations about money are already happening on Messenger, as people chat about bar tabs, splitting dinner bills, and sharing the cost of an Uber ride.

The business model differs from incumbents. Facebook is primarily interested in the transaction data rather than high fees. This is bad news for companies like Western Union and Moneygram, which capitalize on high fees on cross-border transactions in the $500+ billion global remittance market.

For incumbents, the business model should be the biggest reason for concern. In the short-term Facebook Pay will not affect banks and traditional payment service providers other than a new channel for transactions. In the long-term this has two major implications. Facebook acknowledges the future value object in payments is data and customer insight, not transaction fees. If free becomes the market standard, this threatens payments and transcation-banking revenues which is estimated to reach 1 trillion USD in few years.

With Facebook Pay you no longer ned to log on to your bank to transfer money to your friends. This creates additional distance between banks and the customers. Eventually this could render banks as we know it as invisible commodity providers, where all customer interaction is conducted through digital ecosystems like Facebook Pay for payments and e-Commerce, Google Compare for insurance and Google Mortgage for mortgages.

Pingback: A challenger appears in the Norwegian mobile payment space | hernaes.com

Pingback: For those in search of summer reading material | hernaes.com

Pingback: Fintech predictions for 2016 | hernaes.com

Pingback: A short summary of Money 20/20 Europe | hernaes.com

Pingback: The evolution of Facebook | hernaes.com

Pingback: Banks should not underestimate Facebook messenger | hernaes.com

Pingback: Banks should not underestimate Facebook Messenger | Gulf News Today

Pingback: Banks should not underestimate Facebook Messenger - Cool Tech Reviews

Pingback: Banks should not underestimate Facebook Messenger - The News Galaxy

Pingback: Banks should not underestimate Facebook Messenger | EuroMarket News

Pingback: Banks should not underestimate Facebook Messenger - Bain Daily

Pingback: Think and grow wealth Banks should not underestimate Facebook Messenger - Think and grow wealth

Pingback: Banks should not underestimate Facebook Messenger – Technology Craze

Pingback: Banks should not underestimate Facebook Messenger | BizTechPartners

Pingback: Banks should not underestimate Facebook Messenger | Fresh Hot News

Pingback: Banks should not underestimate Facebook Messenger | Tech news home

Pingback: Banks should not underestimate Facebook Messenger

Pingback: Banks should not underestimate Facebook MessengerTech Giant News

Pingback: Banks shouldn't underestimate Fb Messenger

Pingback: Banks should not underestimate Facebook Messenger – Entire News Link

Pingback: Banks should not underestimate Facebook Messenger

Pingback: Banks should not underestimate Facebook Messenger – Viral News Headlines

Pingback: Banks should not underestimate Facebook Messenger - Tech Freak

Pingback: Banks should not underestimate Facebook Messenger | TechNewsDB

Pingback: Banks should not underestimate Facebook Messenger – Find Technology

Pingback: Banks should not underestimate Facebook Messenger – hernaes.com

Pingback: Banks must become open platforms – hernaes.com

Pingback: Will Libra be the killer app of digital money? – hernaes.com